.png "The Building Blocks for AI Long-Haul Networks")

Artificial intelligence is reshaping the economics and architecture of global network infrastructure— and nowhere is that more visible than in the surging demand for high-capacity optical transport. As AI workloads grow in scale and geographic distribution, the long-haul networks that carry them must evolve to keep pace. That evolution is increasingly being defined by one unit of measure: 400 Gbps.

Whether it’s a hyperscaler replicating training data across continents, a neocloud standing up GPU clusters in new markets, or an enterprise accessing frontier models through a cloud API, the underlying requirement is the same—massive, reliable, low-latency bandwidth at scale. 400G wavelengths have become the foundational building block for meeting that demand. Even operators building their own network infrastructure typically start by leasing 400G wavelengths before they reach the scale where owning spectrum or fiber pairs becomes economical.

But the market for 400G is still maturing. Powered by the data in our Transport Networks Research Service, this post examines where the 400G wavelength market stands today, how prices are trending across key global routes, and what buyers and sellers of wholesale capacity should expect through 2032.

400 Gbps Market Trends

Carriers continue to roll out the next step change in capacity, specifically 400 Gbps. While 100 Gbps wavelengths still represent a majority of sales on most key global routes today, providers report that a sizable portion of their sales pipeline within the U.S., Europe, and across the Atlantic is now for 400 Gbps. A smaller number of sales are reported in Asia and across the Pacific. Little to no demand is still reported on routes to Africa, Latin America, and Oceania.

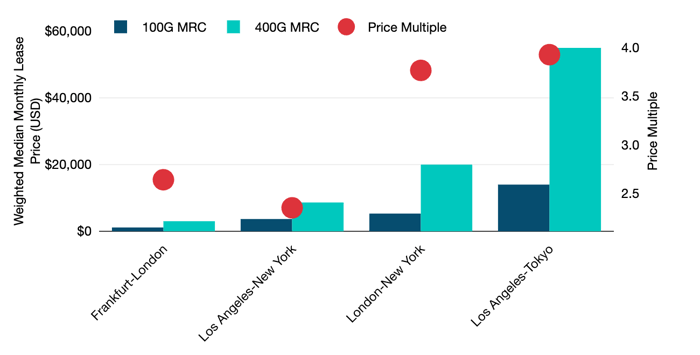

While demand for the service is picking up, there is still only a small discount between 4x 100 Gbps and 400 Gbps. The figure below helps us map this out. Weighted median 100 Gbps prices are represented in the dark blue columns and the 400 Gbps prices in the turquoise. The red dots represent the price multiple for 400 Gbps over 100 Gbps on the listed route.

Weighted Median 100 & 400 Gbps Wavelength Prices & Price Multiples on Key Global Routes

Note: Each column represents the weighted median monthly lease price for an unprotected wavelength for the listed capacity and route in Q4 2025. Prices are in USD and exclude local access and installation fees. Circles represent the price multiple. Price multiples are derived by dividing the price of the larger circuit by the price of the smaller circuit.

As you can see, the multiples between the weighted median 100 Gbps and 400 Gbps prices are lowest on the highly competitive terrestrial routes in Europe, such as Frankfurt-London (2.6). They remain much higher on subsea routes like London-New York (3.8) and Los Angeles-Tokyo (3.9). Individual carrier price multiples for providers who offer both 100 Gbps and 400 Gbps service, ranged from 2.2 to 3.5 on terrestrial routes and from 3.0 to 3.7 subsea. So still a wide range in the market.

Looking solely at the price multiple doesn’t tell the whole story though. Larger savings on install and cross-connect charges as well as power consumption could be compelling factors for some high capacity buyers to shift towards 400 Gbps service. If history is any guide, multiples will continue to compress over time. Terrestrial networks will lead the way, followed by higher capacity subsea routes.

Forecasting 400G wavelength prices

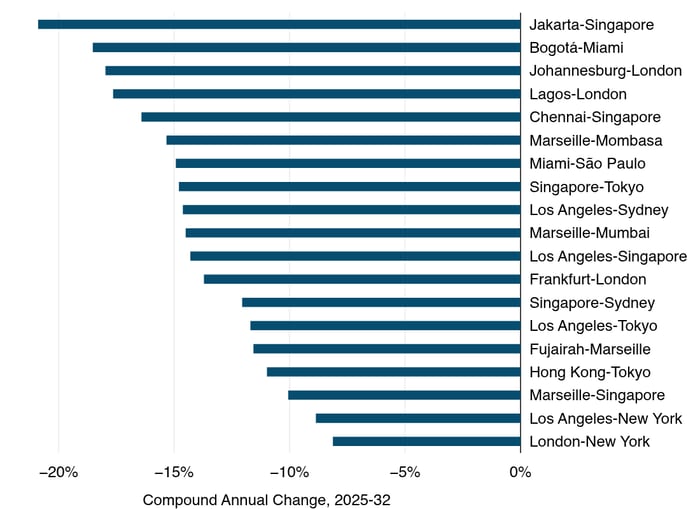

High capacity customers continue to upgrade their networks and sales of 400 Gbps wavelengths continue to increase. With larger volumes, prices continue to fall. Between 2025 and 2032, 400 Gbps wavelengths across key global routes are forecasted to decrease an average of 16% compounded annually, a slightly higher pace than that of 100 Gbps. As 100 Gbps price erosion levels out and demand for 400 Gbps increases, price multiples between the two services will continue to compress.

Forecasted 400 Gbps Wavelength CAGR Price Decline

For all but the very largest users of capacity, leasing wavelengths remains the status quo, as the economies of scale provided by spectrum or fiber pair ownership have remained out of reach. However, higher fiber count cables have the potential to change that by dramatically reducing the cost per bit and making fiber pair ownership far more affordable. Many customers are currently working through when it makes sense to purchase a fiber pair or spectrum instead of leasing wavelengths. But fiber pair pricing is very cable specific and not subject to the same pricing trends we discussed above, which is a big shift for the market.

Hyperscalers have also been increasing their direct ownership in new submarine cables for years. Historically, they have either partnered with service providers in a consortium for those investments or sold fiber pairs to providers, which injected fresh supply and competition into the wholesale market. There are concerns, though, about whether hyperscalers will continue to sell fiber on new systems and if they do, how many pairs per cable will be available. This could potentially limit supply and competition on some routes, curbing price reductions as well.

Despite this, the outlook for the wholesale market is not entirely doom and gloom. Customers are consuming more bandwidth than ever before, particularly with the increasing adoption of cloud services and emerging AI applications. Fulfilling the wholesale requirements for the long tail of capacity users that exists beyond hyperscalers will continue to be a challenging, but critical business going forward.

Get more intelligence like this

Our Transport Networks Research Service delivers data and analysis on long-haul networks and the undersea cable market, with forecasts of international bandwidth supply, demand, prices, and revenues. Learn more and get research samples delivered to your email.

.png&description=The+Building+Blocks+for+AI+Long-Haul+Networks){kind=link}